The world’s biggest economy the United States, which recorded an astonishing GDP of 20.49 trillion was also spearheading the semiconductor industry for over a decade, but things have now taken a turn and the country is now failing to compete with its Asian rivals in assembly and test manufacturing, fabrication, and wafer fabrication. According to various experts, the country lost over 73 percent of share in international semiconductor manufacturing in the last three decades and is now way behind three generations. If no imperative actions are taken, the country would lag behind more that will have serious consequences for its financial strength and also for national security. For instance, of late, Korea has already proclaimed to spend $450 billion into semiconductors while the United States only intends to spend $50 billion into the sector. If the country really needs to become competitive, implementation of revolutionary policies is required in the coming few months.

Other than this, the country has started witnessing threats on its semiconductor industry leadership quite rapidly. An amalgamation of foreign industrial policies and market forces is crafting incentives that are pushing new chip production facilities close to the border. If these kinds of policies continue, then the US might lose its position globally in chip design, equipment, and manufacturing coupled with deadly and imperative outcomes for the country’s economic growth. There are several obstacles attached to the industry’s move, but the European and Asian countries have already started taking care of the challenges in detail and took an important step to research and fund in both process and product technology. There is a new National Research Council Report of the US, which highlighted 16 major initiatives backed by the government at the regional and national level, and as support, a huge volume receives more than $100 million yearly. The country is also home to many global semiconductor manufacturing firms such as Intel, NXP, Texas Instruments, and fabless like Qualcomm and in spite of that, they are failing to strengthen their foothold in the international market share of semiconductor manufacturing.

Highlighting the statement above, Satyajit Sinha - Senior Analyst - IoT Analytics exclusively told CircuitDigest, "Most of the companies in the US depend on China for FAB companies as these companies provide a “node” that is the base component of the chips. And the key FABs companies are TSMC, Global Foundries, UMC, and SMIC. Hence, the dependency on Chinese FAB companies is one of the major roadblocks for US companies. The solution will be to build an in-house semiconductor ecosystem."

"For Example, The European Commission invests 147 billion into semiconductors to develop in-house. Further, last year India approved a $10 billion incentive plan to establish chip and display industries. And currently evaluating the five applications received for setting up semiconductor fabrication and display fabrication units with a total investment commitment of $20.5 billion. In 2017, President Donald Trump and the Wisconsin GOP struck a deal with Foxconn that promised to turn South-eastern Wisconsin into a tech manufacturing powerhouse. However, in 2019 Foxconn will pull back its factory commitment. Hence, the US needs to revisit partnerships and collaboration strategies for building an in-house semiconductor ecosystem," added Sinha.

The Primary Difficulty of Chip Foundries in USA

Ten to fifteen years back, the Asian countries have already commenced operating their foundries and also planned for more in the coming years. It has become possible because the government has assisted the sector with slew of important measures that comprises munificent tax breaks. China took advantage of this situation and has leaped forward matching Taiwan’s initiatives and incentives and then surpassing them with rebates of most of the value-added tax (VAT) on chips crafted or designed exclusively in China. In this massive transformation, the semiconductor industry of China is looking closely at Taiwanese skilled and capital management, and also pulling out investments from the US and various other countries.

Among various imperative policy rollouts, the key one utilized by China in association with regional authorities in Shanghai is easing out taxation structure and rates for skilled personnel, plants, and equipment. Semiconductor, which is a well-known capital intensive country, is benefiting from the rebate of the VAT for Chinese products, which is also showing a sturdy effect. The supreme importance for the US semiconductor industry in the coming years will be dependent on how the policy of the Chinese government will decide its supply base and location base before any steps taken by the US. According to the experts, the USA must undertake instant multilateral and bilateral action to put an end to China’s controversial VAT tariff.

Historically, the USA's leading player in the manufacturing cluster is the semiconductor industry, whose yearly growth rate rose to 17 percent way back in early 90s. Its productivity escalated from 1.5 percent of manufacturing GDP in 1987 to 6.5 percent in 2000. It recorded the largest number of sales in 1999 worth $102 billion. Back in August 2001, this industry helped the country with an employee generation of 2,84,000 people and they were paid an hourly average of 50 percent higher than 30 years back.

Justifying the statement above and pointing out the benefits of the current major policies or steps undertaken by the US government, Tarun Pathak, Research Director at Counterpoint Research exclusively told CircuitDigest, "The Biden administration has brought in the Innovation and Competition Act and intends to spend $52 billion for the semiconductors sector. Further, a 100-day review of the supply chain crunch has been conducted. It covered key semiconductor product lines, advanced batteries used in EVs and regulatory changes as well. Biden has unveiled an infrastructure plan worth $50 billion for the American semiconductor industry as a measure to subsidize domestic manufacturing and chip research. The $50 billion amount is expected to go towards production incentives and research and design, including the creation of a National Semiconductor Technology Center.”

The Bigger Challenges and Market Growth

According to Tarun Pathak, various countries have augmented investments in their semiconductor research and development, while in the US, federal investments in research remained low for many years. The substantial dwindling in the market share of the US international chipset manufacturing due to scanty investments in R&D, showcases the country’s future potential to design, research, develop, and manufacture top-notch chipset needed for the economic assistance, pivotal infrastructure and defense, create new high-wage employment, decreasing price for clean energy technologies, and spearhead growth and innovations in the upcoming advanced technology. To counter this impediment, bipartisan legislation called the CHIPS for America Act was unveiled in 2021. The act permits for investments and incentives in the in-house chip manufacturing and research initiatives, but the point to be noted is that all funding must be carried out via congressional appropriations.

US's R&D spending augmented at a CAGR of approximately 7.2 percent from 2000 to 2020. This investment is always high by the US semiconductor companies, regardless of any cycle in yearly sales. Towards the end of 2020, the total investment in R&D amounted to $44.0 billion, but lacks complete strategic investment for manufacturing.

In an effort to develop more FABs, the US congress is also considering another act, dubbed FABS Act, that would successfully form a semiconductor investment tax credit. Industry experts at the Semiconductor Industry Association mentioned that the Act must be expanded so that it can have a budget for both design and manufacturing to perk-up the complete semiconductor cluster.

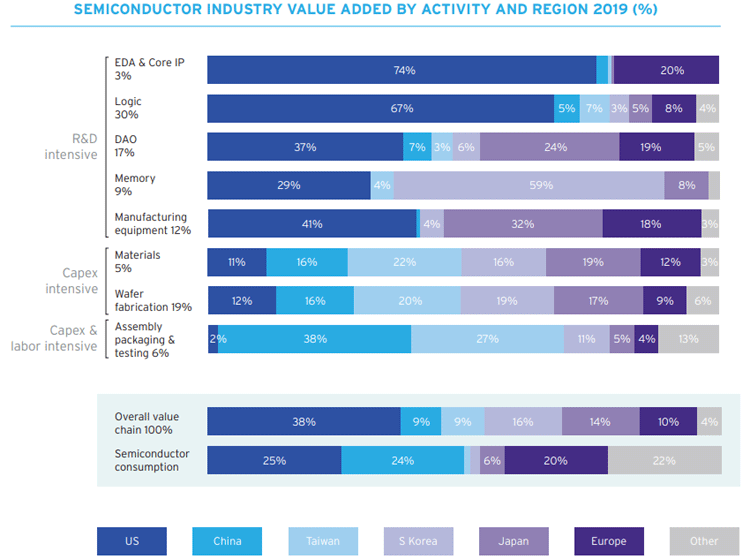

Another interesting fact is that from the latter half of 90s, the semiconductor industry of the US has been a leader in the international market share in sales, which is almost 50 percent of the yearly worldwide market share. Apart from that, it maintained a good momentum in its manufacturing process technology, design, and R&D. For instance, manufacturing and raw materials that includes assembly, test, and packaging (ATMP) and fabrication are mostly done in the Asian countries as they are capital intensive. Around 75 percent of international semiconductor manufacturing is in Asia; including all the leading-edge capacity less than 10 nanometers. This disbalance prompted the US to look out for strategic incentives to boost more manufacturing in the country itself. The US on the other hand is not a leader in manufacturing, but it leads logic and discrete, analog, and opto semiconductors.

Souce: SIA

Being a leader in the domain of design of chipset, the US account for 60 percent of fabless sales all over the world and some of the biggest Integrated Device Manufacturer (IDMs) that craft their own in-house design are also the US companies. On the other hand, the international design workforce is also spearheaded by the US, which showcases the sturdiness of the country’s industry and also the academic ecosystem for semiconductor design. But, amid all efforts it lacks manufacturing leadership in spite of housing the largest chip companies of the world.

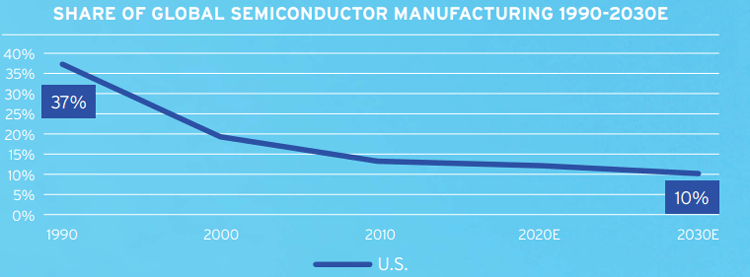

The share of modern semiconductor manufacturing capacity located in the U.S. has decreased from 37% in 1990 to 12% today. This decline is largely due to substantial manufacturing incentives offered by the governments of our global competitors, placing the U.S. at a competitive disadvantage in attracting new construction of semiconductor manufacturing facilities, or “fabs.” Additionally, federal investment in semiconductor research has been flat as a share of GDP, while other governments have invested substantially in research initiatives to strengthen their own semiconductor capabilities, and existing U.S. tax incentives for R&D lag behind those of other countries. Furthermore, global semiconductor supply chain vulnerabilities have emerged in recent years that must be addressed through government investments in chip manufacturing and research. (Robert Casanova, SIA Director of Industry Statistics and Economic Policy noted this in a previous interaction with CircuitDigest.)

The Urgent Solutions to Look For

According to various experts, urgent action is now the need of the hour because the impediment is that no subsidies can help boost the industry, which is spearheaded by volume of wafer that warrants capex and R&D investments to move to the next node in a virtuous cycle. Apart from that, the US should look forward to be cost-competitive with its Asian counterparts based on commercial nodes, where cost is a function of wafer starts given the high fixed cost of equipment. Around 60 percent of wafer cost is depreciation, again showcasing the imperativeness of volume. The large fabrication units have sophisticated equipment capacity matching, and hence, it is equipped with lower costs and high capital efficacy.

Over a decade, the USA has been deprived of having a large foundry in spite of various efforts undertaken by the government and the industry body. Now, when compared to an IDM, foundries are implicitly irrepressible (with a diverse customer base) and are not tied to a particular chip architecture. It has massively affected the country’s market share and manufacturing capacity, especially in the mobile market, which is a high-growth segment. Of late, it lost its mobility market completely to Samsung and Taiwan Semiconductor Manufacturing Company (TSMC). Now, in this regard, the US must give high importance to FABs rather than spending only on R&D labs. For instance, IBM did not unveil that 7 nm HVM in spite of having the intellectual property, whereas GlobalFoundries developed that thing, but it had to throw it away as it failed to get the government assistance in having $3 billion funding required to perk-up production. Hence, the policies must take turn in offering incentives for developing production technology and more incentives must be prioritized for capex investments. The USA must have a daunting share of international yearly semiconductor capex spend of around $105 billion if it wishes to enlarge its manufacturing cluster, which as of now, is only 11-12 percent.