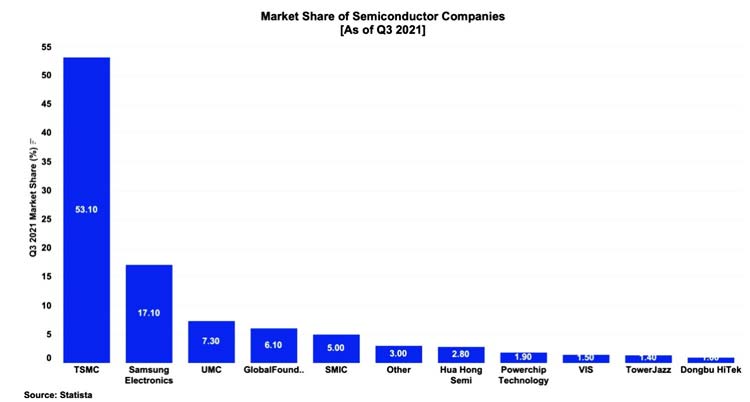

As the Russian-Ukrainian fracas continues, various countries and firms are now busy in evaluating where the upcoming disturbance and disruption in the supply chain will happen. Now, as the financial frictions escalate between China and other western countries, a huge concern over China’s dominating action on Taiwan has augmented. These worries have spotted the requirements of superior visibility of sub-tier supply chains for intricate items like semiconductors, and also the necessity of cleverly expanding the global semiconductor supply chains. Interestingly, in Taiwan, TSMC solely grabbed the vast majority of market share of 53.1 percent, which is then followed by Samsung Electronics 17.1 percent, and UMC of 7.3 percent. It has helped the market share to get concentrated in the region above 60 percent, which according to the experts, the international semiconductor sector’s market share is heavily concentrated in Taiwan. Researchers are also worried that if China manages to grab the entire territory of Taiwan, it will vastly disturb the production of global semiconductors and the supply chain.

If the entire disruptions in the semiconductor supply chain is considered, which obviously the coronavirus is also hugely responsible, the industry was already filled with severe disruptions much before the pandemic stepped in. For instance, the earthquake in the Pacific Rim, cyber warfare, insufficient water supply, lack of top-notch production materials, and power cuts have all put huge pressure on the semiconductor devices. Interestingly, the US China scuffle during the time of the Biden administration increased the price of important goods and also restricted the access to certain items by blacklisted Chinese firms. The Semiconductor Manufacturing International Corp. (SMIC) was also blacklisted in December 2020 for SMIC’s alleged association with the Chinese defense forces, which endangered various chip manufacturers from which the US firms can get their chips. A data from Interos stated that 45 percent of the disruptions have severe effects on the semiconductor supply chain. Moreover, the effect of cyberattacks on TSMC machines in 2018 or the X-Fab Silicon Foundries ransomware attack in 2020, accounted for just 5 percent of all events, but data shows the frequency in the graph increased with the appearance of the COVID-19. In fact, the hacking that was sponsored by the state, like Chinese groups looking to steal other intellectual property to fortify its manufacturing capabilities.

How to Transform the Semiconductor Supply Chain

Ever since the COVID pandemic started creating mayhem across the world, the imperativeness of semiconductors in spearheading economies have increased like never before. Be it the demand blow crafted by the US-China trade war or the COVID-19 virus, the requirement to expand and enhance the semiconductor supply chain has created pressure on the governments all over the world. At the international platforms, the matter is being discussed on a large scale. For instance, the recent one is the Quadrilateral Security Dialogue where the quad members Australia, India, US, and Japan have taken a decision to work jointly to fill the cracks in the semiconductor supply chain.

Another instance in this category is China’s constant efforts to become a global leader in emerging technologies such as AI, 5G internet, and IoT via the recently drafted “China Standards 2035” plan that seeks to build on the “Made in China 2025” plan. According to experts at Counterpoint Research, the current slump in production of semiconductors highlighted worries regarding over-dependence on select countries and markets for important technologies. A lot of developing countries are now working hard to increase their chip productions and become self-dependent, but it is a fact that it takes several years to get it right on the track, especially the needed expense to upgrade and maintain the construction of semiconductor fabrication facilities. Hence, the ideology of self-dependence or self-reliance is not a feasible solution for many because many East Asian countries, US, and EU are assessing their measure to expand and domestically build the semiconductor supply chain to have a seamless network in supply.

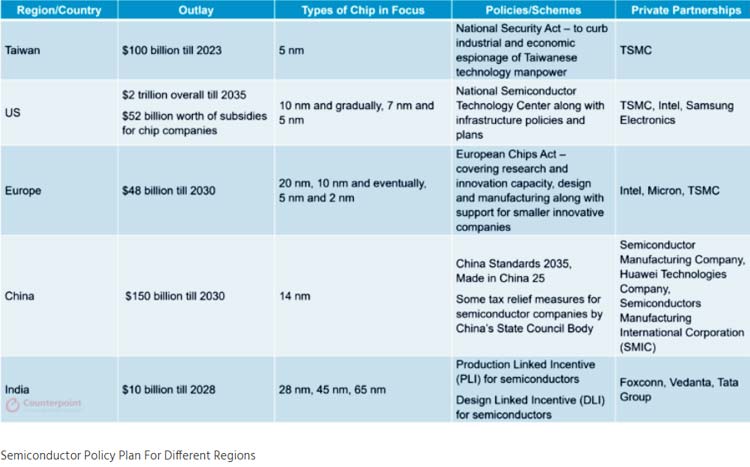

A leading example is Taiwan, which is now the globe’s biggest contract chip maker, and interestingly, it benefited a lot from the international chip shortage. In order to expand its production locations and carry out its superintendence, it plans to invest $45 billion in Taiwan and other countries. Whereas, Taiwan’s competitor the US proclaimed to invest $52 billion on mature nodes production that are utilized largely by the automobile, medical device, agricultural machinery, and defense equipment units. The chip industry in the country has largely supported this plan, which would further provide finance for the upcoming fab units in the country. It will ultimately aid the giant firms like Qualcomm, AMD, and Nvidia that depend on contract chip makers to manufacture their items. The chip manufacturing market in the US reduced to 11 percent from 40 percent in the last 35 years. With this large investment strategy, the US can certainly improve its position in the international supply chain domain.

Now, when the European CHIPS Act commenced, the country intended to escalate its market share to more than two-folds, around 20 percent of semiconductor production towards the end of 2030 with a funding of around $49 billion. Priya Joseph, research analyst at Counterpoint Research said, "The plan of the EU is to craft a new-fangled measure that will assure the security of supply coupled with a special ‘Chips Fund” to center on exports. The highlighted scheme will also have a criteria to pull up exports in case of crises and emergencies. The region is also deploying more than €43 billion in people and private funding to boost larger policy intent around R&D, green transition, and digitization.”

With the help from the “Made in China 2025” plan, China aims to produce 70 percent of semiconductors towards the end of 2025, claims Counterpoint Research. To meet the same, both SMIC and the government of China signed various contracts over the years where the latter will hold a minor share coupled with financial assistance from the local governments. Of late, a lot of industrial policy amendments have been unleashed by China to perk-up the semiconductor cluster via tax exemptions to chip makers. For upto 10 years, corporate and other taxes will be relieved for a manufacturer if it is in function for more than fifteen years and manufactures 28nm or other sophisticated chips.

China’s current rival India recently unleashed the much awaited semiconductor incentive package of Rs 76,000 crore under the Production Linked Incentive scheme. Internationally, worth around $10 billion for six years the policy intends to incentivize all key stages of production of chips like Semi/Display Fabs, Semi ATMP units and Designing. It is one of the most appreciated and out-and-out incentive schemes so far unleashed by the Indian government. There are special exemptions on designing and more than 100 in-house chip designing companies will be boosted by the government under DLI.

Role of Geopolitical Dynamics in Shaping Semiconductor Supply Chain

Amid the various discussions regarding when the semiconductor shortage would come to halt, Counterpoint Research’s latest tracking report stated that during the second half of 2022, the supply and demand gap reduces across most of the components. Since the second half of 2021, the demand-supply gaps have increased that showcased an end to supply across the broader ecosystem. RF transceivers, power amplifiers, and 5G related chips including application processors have escalated significantly during the first quarter of 2022 although the old management 4G processors and power management ICs are still not available widely.

William Li, research expert, who focuses on semiconductors and components said, "We saw OEMs and ODMs continued to accumulate component inventory to cope with uncertainties cropping up from COVID-19 earlier this year. Coupled with wafer production expansion and continuous supplier diversification, we have witnessed significant improvement in the component supply situation, at least in the first quarter. The big risk factor moving forward is the lockdowns happening across China right now, especially in and around Shanghai. But if the government can manage the outbreak and help key ecosystem players turn the corner quickly, we believe the broader semiconductor shortage will ease around late Q3 or early Q4."

According to the global semiconductor experts, in the past few years, the geopolitical dynamics is expected to enhance the market of semiconductors. For instance, the European association of processors and semiconductors is undertaking efforts to bring several EU member states for trade, technology, and research under the semiconductor cluster. The qual alliance on the other hand, playing an imperative role in the Indo-Pacific region, and the recently formed US-EU tech alliance, dubbed the Trade and Technology Council, where France is speculated to lead the semiconductor accord. The biggest differentiating aspect in these efforts will be how beautifully each country uses the amalgamation of finance, knowledge, time, and innovation with the help of domestic and global talent. They will have to work together in such a way that reduces risk during trade outflows and inflows.